How a Single Mother of 4 Is Budgeting for the Holidays in a Year That’s Been Especially Hard on her Wallet

It may seem impolite to talk about money, but if there's any time to tear down that stigma, it's now. COVID-19 has been financially destructive for millions, making budgeting for healthy habits difficult for many, if not almost impossible. That’s where Well+Good’s Checks+Balanced series comes in. Think of it as a space to inspire more open and frank conversations around money—especially regarding how different people are able to afford the wellness habits that are important to them.

The holidays are always a time when budgets are stretched, and many are experiencing a much tighter squeeze this year in light of the pandemic. Here, *Jamie Turner, a 42-year-old therapist and single mom of four living in Kernersville, North Carolina, shares how she's budgeting for the healthy habits that are important to her and holiday gifts for her kids. Keep reading for a complete look at her income and budgeting tips.

Scroll down to see how Jamie manages her finances while budgeting for the holidays during COVID-19.

Jamie, 42, Kernersville, North Carolina

Income: $60,000 per year. My primary job is as a behavioral-health supervisor in a hospital setting. I also have my own private practice on the side, seeing clients outside of my traditional job. Because hospital workers are considered essential, my primary job hasn't changed much during the pandemic, but I have seen a drastic decline in business for my private practice. Unfortunately, many of my clients can no longer afford therapy right now, which has drastically affected my income. Before the pandemic, I was making about $80,000 a year, and now I am making $60,000.

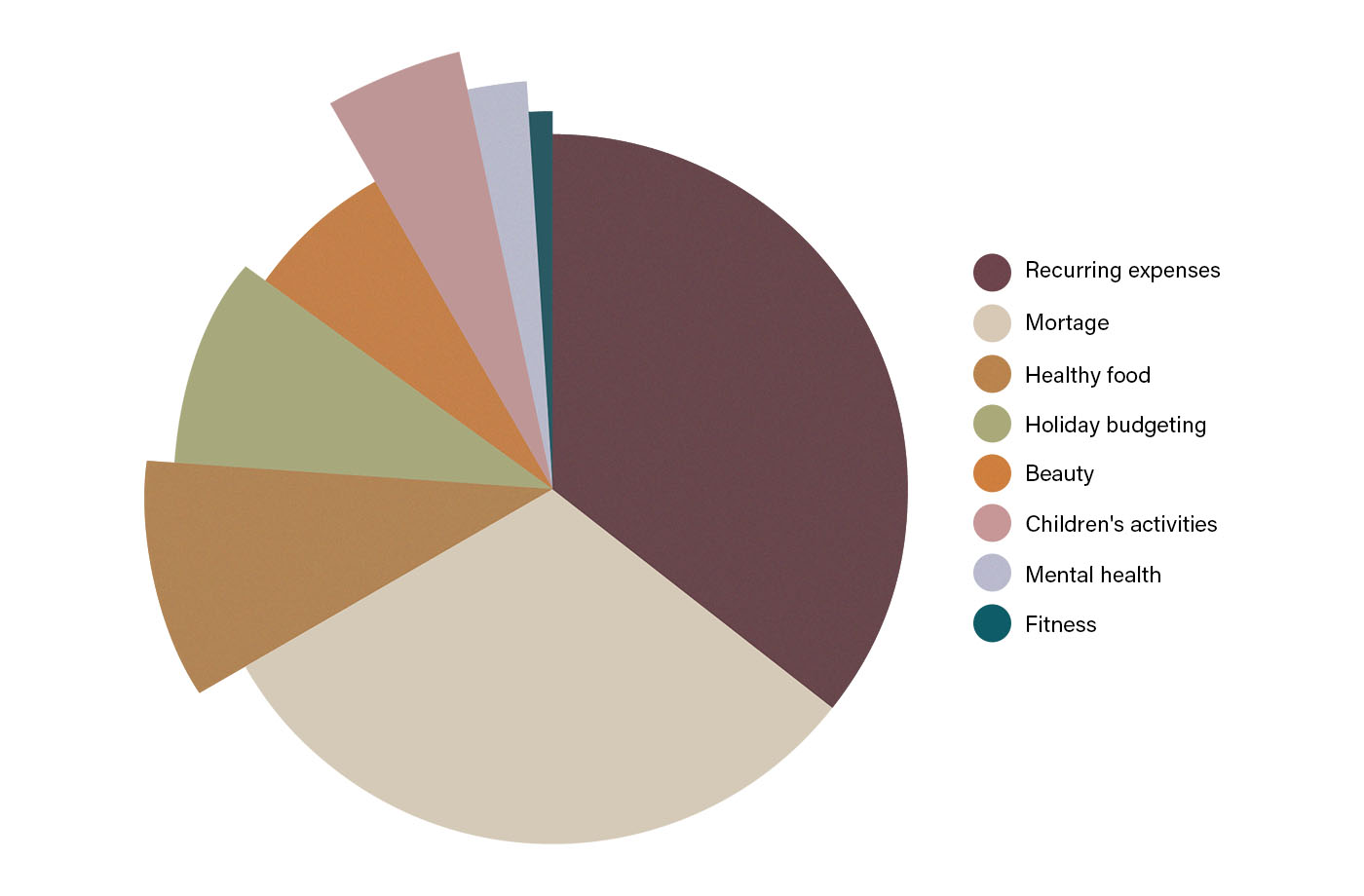

Mortgage: $1,160 per month. I own my home, and my mortgage is $1,160 per month.

Recurring expenses: $1,332 per month. My phone bill is $380 a month, which includes a family plan with all my kids on it. (I have four kids who range in age from 9 to 23, and three of the four live at home with me.) My cable and Internet are one bill, which comes out to $168 a month. I also have a car payment of $476 a month and my car insurance, which is $106 a month. I have a monthly bill for a personal loan, for $270. My utility bill is about $150 a month. I also have a home security system, which is $43 a month. Lastly I have my Netflix bill, which is $9 a month.

Children's activities: $187 per month. I have a few reoccurring expenses related to my kids' activities. My son plays the clarinet in the school band, and his instrument is $37 a month. He's also really into basketball and has an individual basketball coach, which costs $150 a month.

Healthy food: $350 per month. I cook almost all my family's meals at home, and what I make is typically pretty simple: We eat a lot of chicken, steak, hamburgers...things like that. I don't follow any specific type of eating style, but my son doesn't eat pork, so that's the one restriction I really have in the kitchen. I do all my food shopping at Walmart, and I like doing it online so I can see the total as I shop and avoid the sticker shock that can happen at the register. I budget $350 a month for food, and I'm pretty good about sticking to that.

Fitness: $39 per month. Before the pandemic, I used to go to Planet Fitness, which was $10 a month. I also had a personal trainer—unaffiliated with Planet Fitness—which was awesome because it kept me accountable. The trainer was $75 a session. I stopped both my gym membership and training sessions in the spring when everything shut down because of the pandemic. I recently bought a Mirror, which I'm excited about; just last night, my kids and I did a boxing workout together, and it was so fun. It cost $1,495 and has a monthly $39 programming membership, so it will actually save me money in the long run compared to my previous plan at Planet Fitness.

Beauty: $250 per month. I get my hair done every two weeks, which is about $40 an appointment. I also get my nails done every two weeks, which is about $75 each time. Those are my two big beauty must-haves; I'm not really into makeup or anything else. My skin-care products were prescribed by my dermatologist and my insurance covers both the appointments and most of the prescriptions; I just have a $20 copay.

Mental health: $80 per month. Even though I'm a therapist myself, I also see a therapist. This is really important to me for stress-management. My copay for these appointments is $40 a session.

Holiday budgeting: $4,000 per year. I am truly blessed that I have great parents who are a big part of my children's lives and love buying Christmas presents for them. My kids will typically make lists of what they want, and my mom and dad will help quite a bit with the big-ticket items. For my part, I spend on average about $500 for each child, but I also have other people on my list to buy for, including my siblings, nieces, and nephews. All together, I spend about $4,000 each holiday season.

I'll be honest, budgeting for this is difficult, and it's something I think about far in advance. I have a Christmas savings account that helps me save money throughout the year, and I'll buy the presents for my siblings, nieces, and nephews several months in advance. As a mother and therapist, I see all too often how families go into debt and struggle after Christmas. I've learned from that and really try to stick to the budget I set at the beginning of the year. Most importantly, I try not to lose sight of the reason for the season. Especially this year, there's so much to be thankful for that has nothing to do with presents.

*Name has been changed.

If you want to be featured in Checks+Balanced, email emily@www.wellandgood.com.

Oh hi! You look like someone who loves free workouts, discounts for cult-fave wellness brands, and exclusive Well+Good content. Sign up for Well+, our online community of wellness insiders, and unlock your rewards instantly.

Loading More Posts...